This is an update on the mass litigation against appraisers being pursued by Llano Financing Group LLC in relation to loans held or serviced by Impac Funding:

As covered in prior posts, the litigation against appraisers concerning Impac’s mortgages is an unprecedented legal and economic assault on the appraisal profession. For residential appraisers, the Impac/Llano lawsuits are far worse in frequency than the lawsuits filed by the FDIC following the mortgage meltdown and the FDIC’s receivership of more than 500 failed banks. With the Impac/Llano situation, however, it’s remarkable that all the litigation is coming from just one lending source — Impac.

In this new wave of litigation, the investors behind Llano have doubled-down on failed attempts at similar litigation by Heritage Pacific Financial (which is currently in bankruptcy), First Mutual Group LP (who has had 90%+ of its cases dismissed so far), and Savant LG LLC (aka Savant Claims Management), entities which are all connected in some way to an individual named Chris Granter. (Information about the trail of investors who have sued him or the companies affiliated with him over prior failed investments can be found at www.appraiserlaw.com.)

New Case Filings. In August and September, Impac/Llano concentrated new case filings in Illinois, Nevada and New Jersey. It has now filed 50+ cases in Illinois, 35+ cases in Nevada, and 20+ cases in New Jersey. Though the filing of new cases in Florida has slowed, Llano continues to file cases there and has now filed 150+ cases in Florida. Nationwide, Llano has filed 285+ cases for Impac. Because many of its lawsuits name two appraisers, sometimes three, as defendants, Llano has sued more than 450 appraisers and appraisal firms to date. A large number of appraisers have been sued in more than one lawsuit.

|

| Allegation from Llano Complaint: “Agent for Impac” |

Continued Connection to Impac Mortgage. The appraisals at issue in Llano’s lawsuits continue to be connected to loans held or serviced by Impac Funding, which is a corporate affiliate of Impac Mortgage and CashCall Mortgage. According to the complaints, Impac is specifically assigning the legal right to sue appraisers over loans that it holds or services to Savant LG, who then re-assigns them to Llano for litigation as Impac’s alleged agent. In dozens of recent lawsuits, Llano expressly states that it“is suing in its capacity as agent for Impac.” In other lawsuits, Llano also refers to itself and Savant LG as “subservicers” for Impac.

Most recently, legal agreements attached to one of Llano’s court filings indicate that Impac assigned the right to sue appraisers in relation to approximately 7,000 loans of its loans. For that assignment, Impac receives a one-time payment from Savant LG and a percentage of the money that Savant/Llano extract from the appraisers they sue. Impac retains control over the lawsuits by having the right to approve the expenses of Savant LG and Llano for such items as expert witnesses and depositions.

As the word gets out about how Impac has fueled this legal assault on appraisers, some are turning their backs on current appraisal work for Impac Mortgage and CashCall Mortgage. No other lenders — to my knowledge — are currently doing business with Savant or its principals on such a large scale. These appraisers understandably are concluding that a regular appraisal fee is not worth the risk of working for a client who assigns the right to sue appraisers in bulk over defaulted loans and who fuels mass appraiser litigation. Impac has magnified the appraiser’s financial liability risk to a point beyond the realm of any realistic appraisal fee. For the liability risk that Impac seeks to place on appraisers, appraisers might need to charge $1,000 or more per appraisal for Impac (or its CashCall subsidiary) and then allocate most of that increased fee to saving for the costs of the inevitable lawsuits and higher insurance premiums that will result from Impac’s tactics.

As the word gets out about how Impac has fueled this legal assault on appraisers, some are turning their backs on current appraisal work for Impac Mortgage and CashCall Mortgage. No other lenders — to my knowledge — are currently doing business with Savant or its principals on such a large scale. These appraisers understandably are concluding that a regular appraisal fee is not worth the risk of working for a client who assigns the right to sue appraisers in bulk over defaulted loans and who fuels mass appraiser litigation. Impac has magnified the appraiser’s financial liability risk to a point beyond the realm of any realistic appraisal fee. For the liability risk that Impac seeks to place on appraisers, appraisers might need to charge $1,000 or more per appraisal for Impac (or its CashCall subsidiary) and then allocate most of that increased fee to saving for the costs of the inevitable lawsuits and higher insurance premiums that will result from Impac’s tactics.

Early Losses and Errors by Impac/Llano. The good news is that Impac/Llano — like the losing investors before it — probably will not succeed. They already has lost several early cases based on clear defenses, such as statute of limitations, that can be raised successfully at the outset in some cases or because of other missteps by its legal team. However, since most of the cases are very new and the appraisers are just being served with the complaints now, it will be several months before we see the result of the many upcoming motions to dismiss. When newsworthy and helpful decisions occur, and for as long as the lawsuits continue to burden appraisers insured by LIA, I will prepare updates so that appraisers and their legal counsel can have access to the most current legal developments in defending claims by Impac/Llano.

Recent missteps have included suing the same appraiser in different lawsuits about the same appraisal. In one instance, First Mutual Group first sued the appraiser contending that it was assigned the claims by Impac, but Llano later sued the same appraiser claiming it owned the claims. Actions like these lead us to wonder whether they just create new paper assignments whenever they want a different version, while the investors who apparently bought the claims from Savant LG might be asking themselves: “What did we actually buy?”

Another notable misstep by Llano (other than filing hundreds of weak cases that they will likely lose in the end) has been to attach highly personal consumer records pertaining to borrowers on loans held or serviced by Impac. In one case in Illinois, Llano — acting as Impac’s “agent” — actually attached a complete, unredacted credit report for the borrower on Impac’s loan. Aside from being a serious violation of the borrower’s privacy rights, the glimpse into the creditworthiness of the borrower in that case shows that Impac was very willing to buy or fund a loan to a borrower with poor credit and then blame the appraiser for its loan loss. It exemplifies why Impac itself — despite having assigned the claims out to its “subservicers” Savant LG and Llano — and Impac’s own lending practices will very much be on trial if these cases go forward.

It was poor judgment by Impac, likely made without adequate due diligence, to release private consumer records of borrowers to Savant LG and its operators and affiliates, given their prior track record. Llano’s publication of the borrower’s credit report in the Illinois case exemplifies real harm flowing from that poor judgment.

|

| Partial Copy of Cash Flow Prediction Offered by Investment Broker in 2014 |

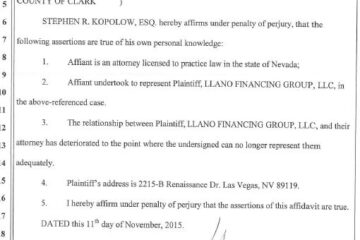

How Many Appraisers Will Impac/Llano Sue? They give no direct indication of the answer. As mentioned above, Impac granted the right to sue appraisers over as many as 7,000 loans (approximately), but we don’t know how many cases Impac/Llano will actually decide to file. Third-party promoters of the initial “investment opportunity” to sue appraisers perhaps have provided a clue. In 2014, the promoters distributed financial projections to proposed investors. They were not savvy about whom they forwarded those projections to and sent them to investors burned earlier in similar ventures — the burned prior investors forwarded those projections around to get the word out and express their frustration. In those projections (a partial copy of one spreadsheet containing the projections is attached here), the investment promoters suggested that the first tranches of the business plan would involve filing as many as 100 cases per month for a period of 20 months, meaning that 2,000 cases would be filed if that particular plan were followed by investors. Llano is not far under that pace with its Impac-related lawsuits. And, of course, if the first round of 2,000 cases somehow succeeds (against the odds), new rounds would follow.

E&O Insurance Issues. I recently was forwarded an email that the president of a state appraiser group sent to the group’s members. The president of the group wrote in her email: “Many E&O companies have settled to avoid court proceedings.” Fortunately, I don’t think that’s actually happening. I see no evidence that any insurers in general have been seeking to settle any claims filed by Llano so far. For LIA, however, I can affirmatively say that our appraiser E&O program has not paid a dime in settlement or damages on any lawsuit or demand by Impac/Llano and that our program will seek to make Impac/Llano prove the validity of each and every legal claim they make. These parties are wasting their money filing their weak or frivolous claims against the appraisers insured in LIA’s program.

On the matter of insurance, I do unfortunately hear from appraisers outside of our program who reach out to me for assistance because they do not have E&O coverage for their defense. The most common reasons why appraisers do not have coverage for claims by Llano are: (1) the appraiser being sued signed the report as a supervisor and has one of the E&O policies that exclude supervision of other appraisers/trainees/contractors; (2) the appraiser did the appraisal as a trainee and did not have coverage under the supervisor’s policy or have his or her own coverage; (3) the appraiser made a switch to an E&O policy without prior acts coverage (the concept of “prior acts” coverage is explained in this post here); or (4) the appraiser discontinued his or her E&O coverage and did not obtain “tail” coverage. Regardless of any appraiser’s insurance coverage situation, I would suggest that appraisers sued by Llano get legal counsel and defend the case. Don’t allow Llano to win a default by your failure to show up — these cases can be defended efficiently.

Long term, if the type of litigation that Impac has spawned here endures despite the odds, it would be inevitable that appraisers’ insurers would move to a framework of generally excluding coverage for appraisals for specific lenders like Impac that create economically unsustainable legal risk and/or charging very significantly higher premiums for those appraisers who specifically want to work for such lenders. This is what occurred in Australia when appraisers were faced with voluminous litigation by lenders and mortgage insurers; if appraisers needed coverage for the types of claims being brought by those parties, the premiums for coverage often exceeded $25,000 per year. Even now, it is rapidly becoming difficult for appraisers who have been sued by Impac/Llano to secure insurance at renewal because of the likelihood that the appraiser will be sued in multiple cases.

Beware of Appraiser Karma. In our world of claims involving appraisers, we quite often see different versions of this same story — in this version of the story, an appraiser did a review appraisal that was used by Savant LG in a currently pending case against another appraiser in Florida. That same appraiser later found himself named as a defendant in a lawsuit filed by the related entity First Mutual Group LP. That is appraiser karma at work. More seriously though, I do encourage that appraisers think about how their appraisal work — particularly, appraisal review work — is used by their clients and, when that work is going to be used by operators like Savant LG, First Mutual Group or Llano Financing to destroy the livelihoods of their colleagues and increase the financial burden on all appraisers through higher risk and insurance costs, I think it’s a reasonable suggestion that appraisers turn down such work — if only because our experience confirms that “what goes around, comes around.” Indeed, according to a person who actually works for these litigation entities, one appraiser even did a review of his own prior appraisal and that review was used to substantiate the lawsuit against him or her. Most of the review work, however, that these parties have been using actually is being done by an appraiser in Texas (according to the same party working for these entities). Aside from geographic competency, one of the troublesome issues with that is that the reviews are of appraisals of properties in other states, including Florida which requires that appraisers be licensed there in order to do a review of an appraisal of a property in Florida.

Peter Christensen is an attorney who advises professionals and businesses about legal and regulatory issues concerning valuation and insurance. He also serves as general counsel to LIA Administrators & Insurance Services. He can be reached at peter@liability.com.